Sorry, this activity is currently hidden

Section outline

-

Introduction

This section establishes how an audit firm’s quality management strategy drives consistent engagement performance and credible audit opinions. You will connect the evolution of quality thinking to modern governance and leadership expectations in financial audit. The focus is on aligning quality with audit objectives while reinforcing a culture of ethics and professional skepticism.

Learning Objectives

-

Differentiate major quality management paradigms and explain how they shape audit quality strategy.

-

Evaluate governance, accountability, and leadership models for their impact on audit quality outcomes.

-

Align quality strategy elements (culture, ethics, skepticism) to financial audit objectives and execution.

-

-

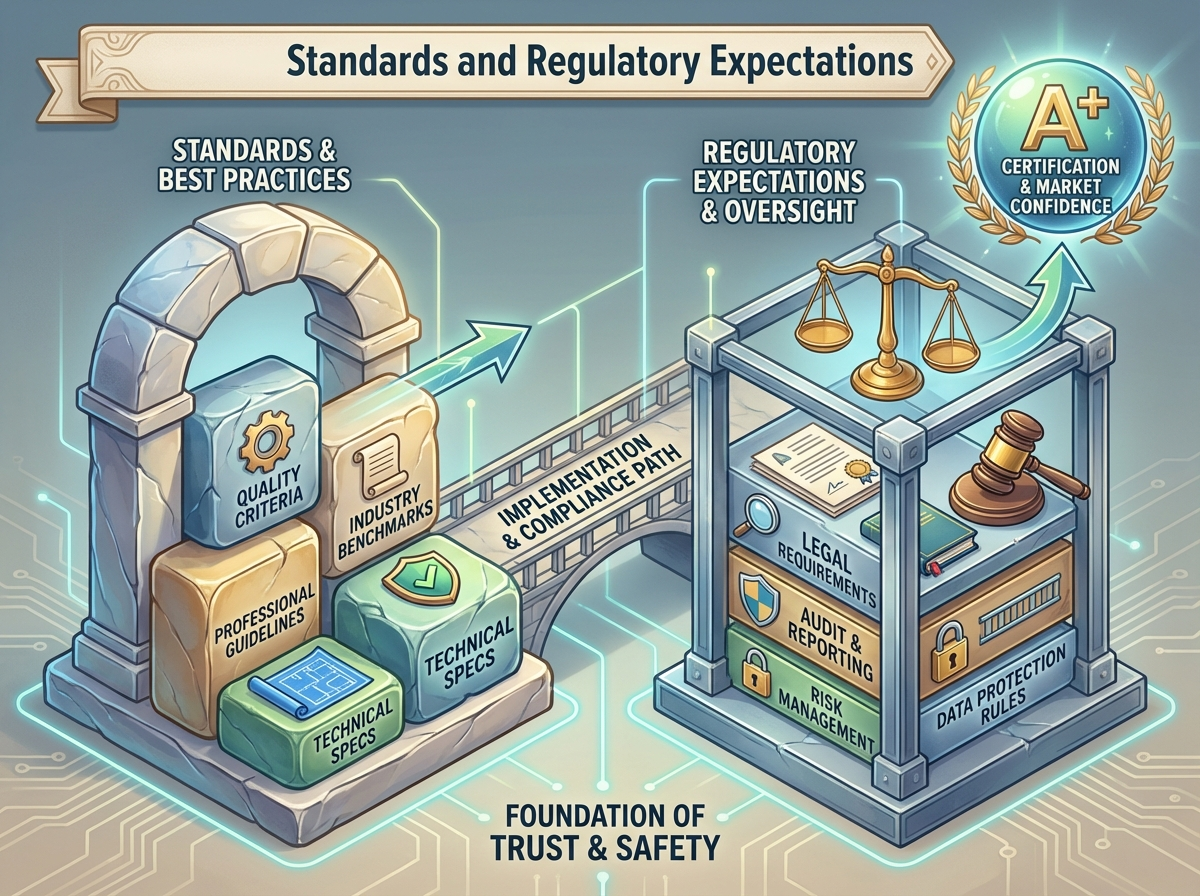

Introduction

This section connects quality management frameworks to the specific standards and regulatory expectations that shape financial audit performance. You will translate ISO-style QMS concepts and IAASB quality management requirements into practical, auditable firm and engagement-level practices. The focus is on what regulators look for: credible evidence, traceable documentation, and controls that protect independence and objectivity.

Learning Objectives

-

Map core ISO 9001 concepts to policies and processes that support audit quality in practice.

-

Interpret IAASB quality management standards and apply their intent to firm and engagement responsibilities.

-

Design documentation and independence controls that meet regulator expectations for traceability and evidence credibility.

-

-

Introduction

Risk-based quality management is how audit firms translate quality intent into specific, prioritized actions across the engagement lifecycle. In financial audit, this approach helps prevent systemic breakdowns in judgments, supervision, and evidence gathering that can lead to inspection findings and audit failures. This section focuses on identifying quality risks early, calibrating responses to risk appetite, and using indicators to detect emerging issues before they become deficiencies.

Learning Objectives

-

Identify and categorize quality risks across the audit lifecycle and link them to likely failure patterns.

-

Set and apply risk appetite, tolerances, and performance targets to drive proportionate quality responses.

-

Design practical controls and indicators to mitigate engagement risks and provide early warning signals.

-

-

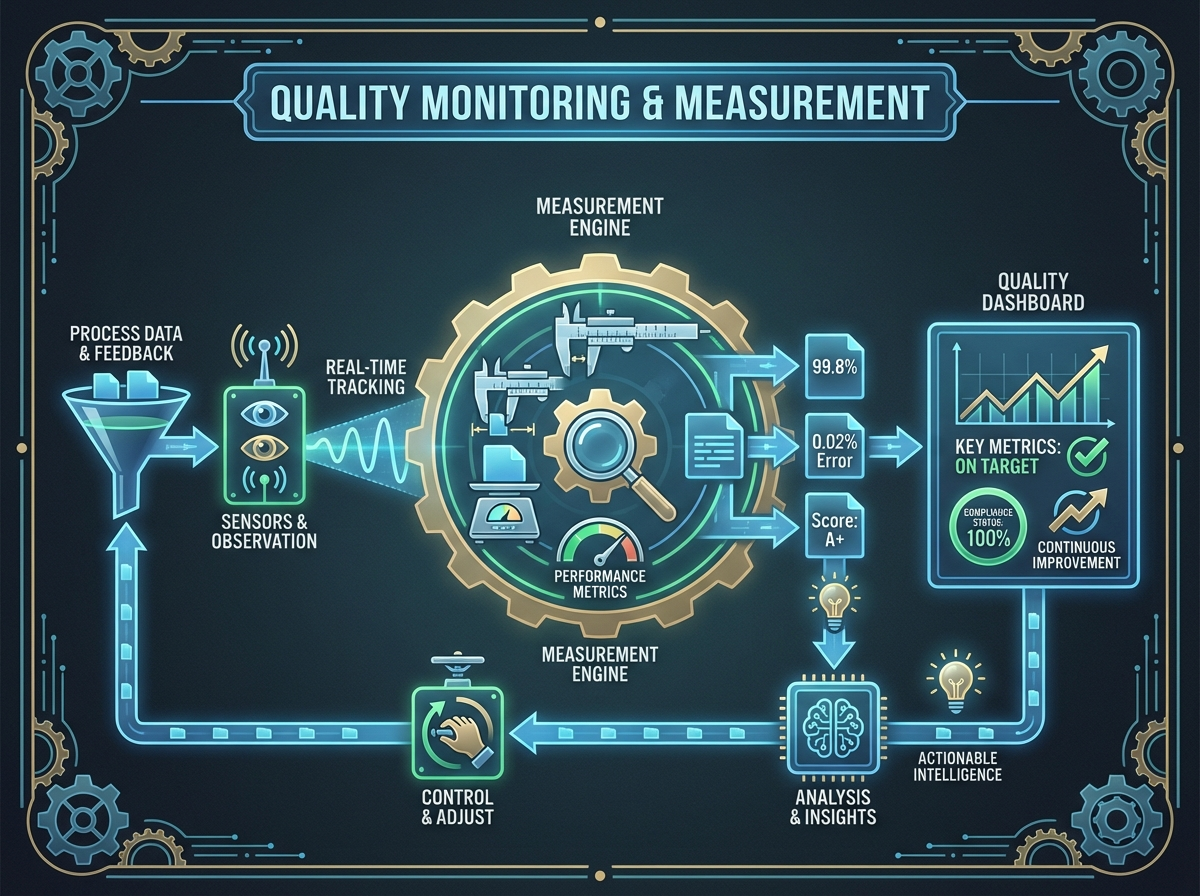

Introduction

Effective quality management in financial audit depends on how well quality is monitored, measured, and acted upon. This section focuses on building monitoring programs that surface meaningful signals, distinguish real performance from noise, and drive timely remediation. It connects measurement choices to inspection outcomes, regulatory scrutiny, and reliable audit evidence.

Learning Objectives

-

Design a fit-for-purpose audit quality monitoring program and dashboard aligned to firm and engagement risks.

-

Define and apply audit-relevant KPIs that avoid vanity metrics and support defensible conclusions.

-

Evaluate deficiencies using consistent grading, escalation, reporting, and continual improvement practices.

-

-

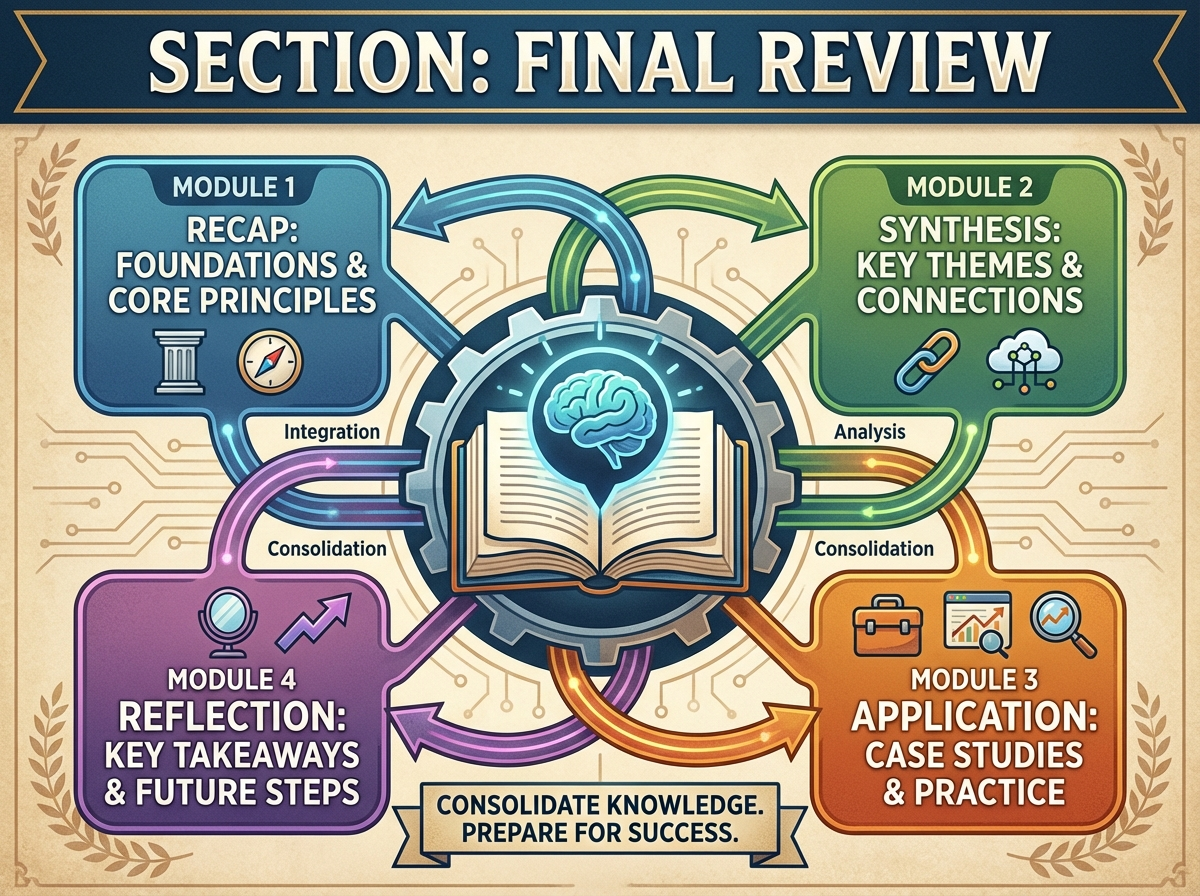

Introduction

This final section consolidates the course’s advanced quality management concepts into a coherent, audit-ready perspective. It focuses on how quality strategy, standards, risk-based thinking, and monitoring connect to strengthen financial audit execution and outcomes. You will also translate key takeaways into practical next steps for continued capability building and professional development.

Learning Objectives

-

Synthesize the course’s quality management concepts into an integrated view of audit quality.

-

Evaluate personal and team priorities for strengthening quality behaviors, ethics, and professional skepticism.

-

Identify targeted next learning steps aligned to standards, regulator focus, and firm quality objectives.

-