Sorry, this activity is currently hidden

Section outline

-

Introduction

In this section, you will gain a foundational understanding of securities markets, essential for anyone entering the fields of banking, broking, or asset management. This knowledge is crucial as it sets the stage for more advanced topics such as securities lending. Understanding the types and roles of securities and the key players involved provides a backdrop for comprehending the dynamics of financial markets and how securities borrowing and lending fits within these frameworks.

Learning Objectives

- Identify and describe the different types of securities, including bonds, stocks, and others, used in financial markets.

- Explain the role of securities in financial markets and how they contribute to the economy.

- Recognize the key players in securities markets, specifically banks, brokers, and asset managers, and their functions.

-

Introduction

In this section, we'll explore the fundamentals of securities lending—a critical aspect of the financial markets. Understanding securities lending is essential for professionals in banking, broking, and asset management, as it plays a pivotal role in providing liquidity, facilitating hedge funds, and contributing to the efficiency of financial markets. By grasping its purpose and benefits, you'll be better equipped to make informed decisions and optimize strategies in your professional roles.

Learning Objectives

- Define securities lending and outline its historical development.

- Identify the primary purposes and benefits of engaging in securities lending.

- Recognize and understand key terminology and concepts within securities lending.

- Describe typical transactions and processes involved in securities lending.

Lesson Structure

Lesson 1: Definition and History of Securities Lending [20 minutes]

Lesson 2: Purpose and Benefits of Securities Lending [20 minutes]

Lesson 3: Key Terminology and Concepts [10 minutes]

Lesson 4: Typical Transactions and Processes [10 minutes]

Total: 60 minutes

Verification:

- The sum of lesson times (20 + 20 + 10 + 10) matches the section duration of 1 hour.

- The number of lessons (4) is appropriate for a 1-hour duration, providing adequate time for each topic while keeping sessions concise.

- The lesson sequence builds progressively from foundational history and definitions to more complex transactions and processes.

- Lesson titles align with the course outline points outlined for Section 2.

-

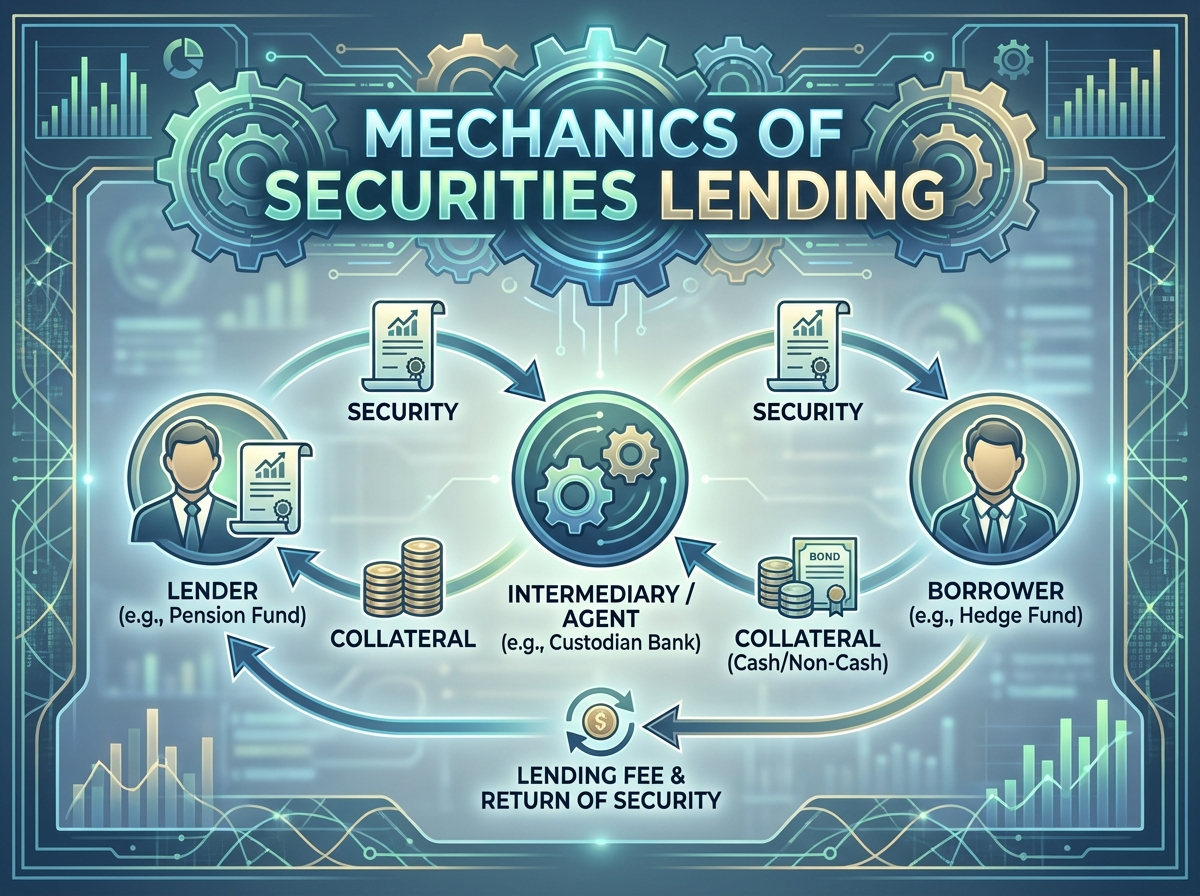

Introduction

In this section, you will gain an understanding of the mechanics behind securities lending, which is a critical component for the efficient functioning of financial markets. This knowledge is vital for professionals across banking, broking, and asset management sectors, as it plays an integral role in facilitating liquidity, reducing transaction costs, and enabling hedging strategies. Comprehending these mechanics is essential for anyone aiming to participate in or manage securities lending activities successfully.

Learning Objectives

- Explain the detailed process of securities lending, including the roles of lenders, borrowers, and intermediaries.

- Identify and analyze the requirements and significance of collateral in securities lending.

- Assess risk management practices and comply with regulatory frameworks in the context of securities lending.

-

Introduction

In the highly dynamic fields of banking, broking, and asset management, understanding securities borrowing strategies is crucial for leveraging opportunities in diverse market conditions. This section introduces you to the strategic use of borrowed securities, specifically focusing on borrowing strategies, the objectives of short selling, and their application in asset management. This knowledge is pivotal for optimizing portfolios and managing risks effectively, providing a competitive edge in the financial industry.

Learning Objectives

- Understand the fundamental borrowing strategies employed in securities lending and their relevance to market operations.

- Explain the motivations and methodologies behind short selling, including its risks and potential rewards.

- Explore the strategic use of borrowed securities to enhance asset management practices and outcomes.

-

Introduction

In this concluding section of the course, we will consolidate and review the key concepts covered throughout the program. This section is crucial for reinforcing your understanding of securities borrowing and lending, providing a foundation for future learning and application within the banking, broking, and asset management sectors. By synthesizing the information learned, you will be better equipped to apply these concepts in real-world scenarios, enhancing your professional competence and decision-making capabilities.

Learning Objectives

- Recap and reinforce the core principles and concepts of securities borrowing and lending.

- Identify the practical applications and implications of these concepts in the banking, broking, and asset management sectors.

- Outline pathways for further learning and professional development in the domain of securities markets.